Amortisation and Financial Regulation in European Football

Is Chelsea's strategy genius, exceesive risk taking or a bit of both?

Following UEFA's announcement of its Financial Sustainability Regulation (FSR), football executives and other stakeholders commented on how it would impact club operations and investment in the industry. (You can view my brief analysis of the FSR here). A year after FSR's introduction and one season before the regulation would come into force, Chelsea's transfer activities are in the headlines. Reportedly, Chelsea has spent upwards of £400m in the transfer market in the same financial year (two transfer windows). How is this possible? Are there any risks? Does UEFA need to react? I'd provide a few thoughts here – brace yourself, this might be a bit technical for non-finance readers, but I'd try to keep it simple.

Amortisation in the Profit or Loss Statement

An important feature in Chelsea's recent transfer activity are the unusual contracts lengths that the purchased players signed to. Generally, players sign contracts for between four and five years, but Chelsea's recent signings have signed seven or eight-year contracts. Based on accounting standards, purchased assets should be recognised in the profit or loss (P/L) statement over the asset's useful life, regardless of payment structure. For example, suppose I buy a car for £4m, and based on historical precedent, I believe the useful life will be four years. I would record £1m in my P/L statement in years one through to four, even though I paid £4m for it in year one (Please note that I can structure the payment over, say, two years instead, I will come to this). If I believe I will use the car for eight years, I will record £500k instead of £1m. Exchange the car for a football player's contract and re-read.

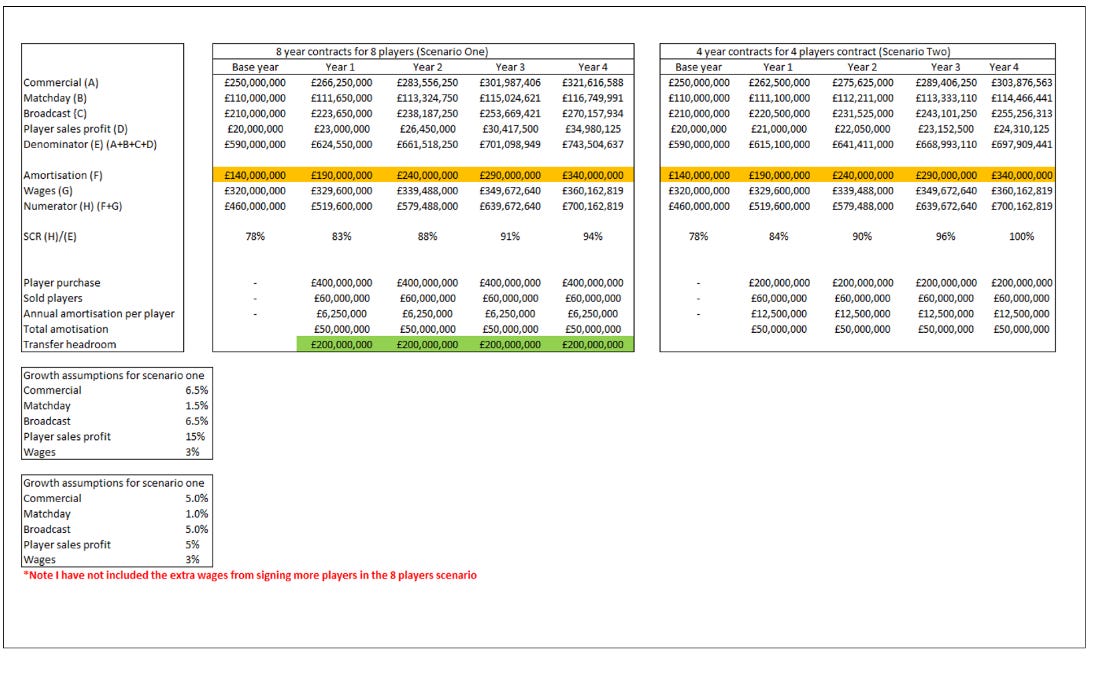

In the tables below, I have constructed a fictitious Squad Cost Ratio analysis (refer to the FSR article) using two scenarios; eight and four-year contract strategies. While fictitious, they aren't far off what you will find at a top club. Also, the growth assumptions are not far from what you would see at a club.

Notice that the SCR for both scenarios are identical even though in scenario one the club signed eight players on eight year contracts compared to the four players on four year contracts in scenario two. Also, the amortisation value was the same. "Loophole", right? Let us see.

Amortisation in the Balance Sheet (P/L inclusive)

When a club buys a player, asides from recognising the transaction in P/L, the purchase price is recorded in the balance sheet as an asset. The annual amortisation value is deducted from the purchase price and recorded as the closing book value. The higher the amortisation, the lower the closing book value. Also, when a player is sold, the profit recognised in the P/L is the difference between the sale price and the book value. What is the potential impact of scenarios one and two? See the tables below. (Please note that while I have analysed the potential implications for one player below, remember that scenarios one and two have eight and four players, respectively).

From the tables above, it is clear that the closing book balance in the balance sheet is higher for scenario one, while the amortisation charge – which goes to the P/L – is higher in scenario two. I have assumed that the club and the player agree to a new five-year contract in year three (this is normal as he'd have had only one year left on the initial contract). If the player has performed well (Regardless of contract length) and sold in year four, scenario two "earns" more profit than scenario one, even though the total amortisation cost is higher. While the net effect of the transaction is £0, the club reported less cost in scenario one between years one and four.

A key thing to note is that if the player was sold in year seven the sales price will be the total profit for scenario two while in scenario one, the club would have to sell the player above £6.25m to break even. Also, if the player isn't sold, the club's transfer budget in scenario one would be £6.25m less than in scenario two. Another silent implication is that scenario one would be amortising more costs into the P/L in years five to eight than scenario two. Thus, this would impact their transfer budget wiggle room in those years.

Transfer Fee Payment(s)

Remember the example I gave about the car? Assume you can pay in instalments rather than at once. Let's do the same for football players. It isn't easy to estimate the length of repayment that clubs agree to, but it would be erroneous to think it can stretch as long as, say, eight years. Based on my experience in analysing clubs' financial statements, I believe two years is prudent. However, for this article, I have assumed four years. It is important to note that UEFA requires clubs not to have overdue payables (creditors), and they vigorously monitor them.

The line "additional benefit from strategy" is an estimation of football-related income that the club might have from having the additional players. This might include ranking higher in the League table, increased commercial income from better performance and improved matchday revenue from progressing further in Cup competitions. These additional benefits are conservative but would not differ from actual figures. Also, it is important to note that I have not included cash from the sale of players. See the tables below for the basis.

I excluded additional cash from player sales because modelling transfer fees is an extreme sport. However, the extra cash required for scenario one can serve as a guide to the minimum transfer fees they must receive from selling players for the strategy to work. It is important to note that in football, transfers don't always go as planned, nor do players always develop as expected. Also, another assumption is that the club can achieve constant progress in the League and Cup competitions, which isn't always the case, despite investing in the playing squad.

(Potential) Regulatory Impact

It could be said there isn't a blatant infringement of the FSR, as there is no specific guideline to a maximum contract length. However, UEFA constantly interacts with clubs to clarify grey areas. Nevertheless, with UEFA's President asserting that the FSR's objective is to protect the industry and "prepare it for any potential future shocks while encouraging rational investments and building a more sustainable future for the game", It wouldn't be out of place to think UEFA might address this issue soon.

Another thing to think about is whether what Chelsea is doing contravenes accounting principles. There is a principle called substance over form in accounting, which requires a company to report the economic substance rather than the legal form of a transaction. The question then is, can Chelsea or another football club show that football players generally stay at one football club beyond five years? Think about the football club you support. How often does this happen? I'm sure auditors, in addition to UEFA, would be keeping a close eye on this new trend because they assess industry norms when determining the reasonableness of amortisation years.

Player Impact

For players, a potential benefit of a long-term contract is stability and assurance of future wages. At the same time, it can restrict their power to force a transfer to another club if their current employer insists on an excessive transfer fee. Harry Kane can attest to this. Also, the player would not have the bargaining power to demand a new contract at higher wages, as Mo Salah did with Liverpool last year. This is why players generally seem happy with four-year contracts with the option of an extra year. Time will tell if players prefer the option of longer term contracts (Side note, the long contracts could also have incremental wage clauses).

Conclusion

Chelsea's recent transfer activity has sparked conversations on the strength of UEFA's FSR, with commentators and fans criticising the "loophole". However, it is essential to note that regulation is an ongoing activity that requires changes. Nevertheless, the strategy is neither air-tight nor fail-proof though it allows the club to heavily invest in its squad in the short-term. However, it is a high-risk strategy even in the high-risk football industry, where until recently, football clubs have recorded significant financial losses. Will UEFA react with an addendum to the FSR or issue a guideline? Will other clubs follow suit? I'm sure the coming months will be engaging in the ever-interesting moving regulator and regulated relationship.

Would love to hear about J League finances, like how Kashima Antlers signed Zico

https://hiddenjapan.substack.com/p/the-kashima-antlers-origin-story